Kalinski: The one statistic every renter needs to see

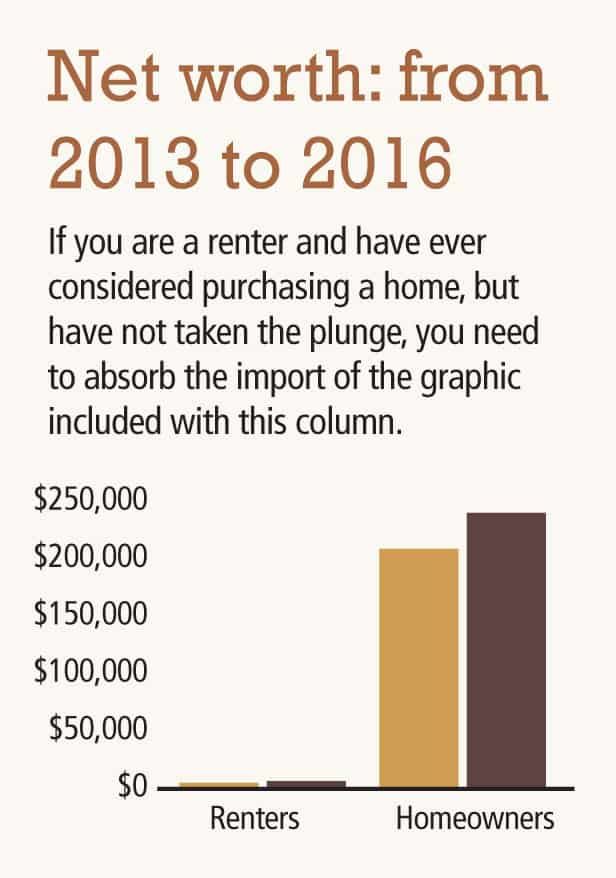

That’s right, based on the latest available data from the Federal Reserve Survey of Consumer Finances, the average net worth of a homeowner is $231,000, a whopping 44 times greater than the average renter’s $5,200 net worth. What makes the situation more dire is the fact that the gap is widening. From 2013 to 2016, the average net worth of homeowners increased 15 percent while the average net worth of renters decreased by 5 percent. The situation for renters is bad and getting worse.

That’s right, based on the latest available data from the Federal Reserve Survey of Consumer Finances, the average net worth of a homeowner is $231,000, a whopping 44 times greater than the average renter’s $5,200 net worth. What makes the situation more dire is the fact that the gap is widening. From 2013 to 2016, the average net worth of homeowners increased 15 percent while the average net worth of renters decreased by 5 percent. The situation for renters is bad and getting worse.

More than any other factor I could identify, homeownership best explains the gap between the haves and have nots. People seem to understand this fact, as a Gallup poll showed that Americans chose real estate as the best long-term investment for the fourth year in a row. So, why aren’t more renters buying homes?

Desire?

SPONSORED CONTENT

How Platte River Power Authority is accelerating its energy transition

Platte River Power Authority, the community-owned wholesale electricity provider for Northern Colorado, has a history of bold initiatives.

It could be that renters do not want to own homes. Anecdotally, we hear stories about how Millennials prefer to rent to give them a more flexible lifestyle, but the research tells a different story. In fact, Millennials represent the largest share of homebuyers today and only 7 percent of respondents to an NAR survey said that they did not want the responsibility of owning. More generally, 82 percent of renters expressed a desire in the fourth quarter of 2017 to be homeowners and about the same percentage said that homeownership is part of the American Dream.

What is driving this desire for renters to become owners? According to a recent survey, the main reasons renters would want to buy a home are: a change in lifestyle such as getting married, starting a family or retiring; an improved financial situation; and a desire to settle down in one location.

Renters seem to know that owning a home is a great investment, and they overwhelmingly express a desire to do so, and yet something is preventing many of them:

Ability

Based on a recent NAR survey, it appears that ability (perceived or actual) is the biggest obstacle to homeownership. In fact, 66 percent of renters reported that it would be somewhat or very difficult to save for a downpayment on a home. Only 16 percent said that it would not be difficult at all. Of those who said saving for a downpayment was difficult, 49 percent identified student loans, 42 percent cited credit card debt, and 37 percent cited car loans.

The above, however, only focuses on one aspect of home affordability. Another side is home price appreciation. That is, if homes were more affordable, it would be easier to save for a downpayment. Unfortunately for local renters, Boulder County has appreciated more since 1991 than any other area in the country — more than 380 percent! The average single family Boulder County home topped $708,000 in February 2018, which is almost 20 percent higher than two years ago.

In addition, interest rates are on the rise in 2018, and we’ve already covered how a 1 percent increase in interest rates can reduce your purchasing power by 10 percent.

Takeaways

There are two takeaways from this. First, for renters, you may be familiar with the adage “The best time to buy a home was 30 years ago. The second best time is now.” That is true now more than ever. If you have been considering making the jump to homeownership, now is the time. At this point, each day delayed likely equals less home for the money.

Second, for local government officials, if you truly support the idea of affordable (market rate) workforce housing, you have the power to encourage it. Without you, the affordability situation will only continue to deteriorate.

Jay Kalinski is broker/owner of Re/Max of Boulder.