Some banks reach limits of real estate lending

Despite reports of shrinking commercial real estate lending opportunities, the industry in Northern Colorado is robust, according to bankers in the region.

Despite reports of shrinking commercial real estate lending opportunities, the industry in Northern Colorado is robust, according to bankers in the region.

Matt Gorr, chairman of First Western Trust in Boulder, said the economy is seeing a number of financial institutions in the commercial real estate marketplace nearing capital restriction levels, which then is going to diminish the opportunity to fund loans as readily as they have been funded since the Great Recession.

“Financial institutions specific to our market in Boulder and Boulder County have been able to expand commercial lending portfolios primarily on the back of funding non-owner occupied state loans — basically investor real estate,” Gorr said. “It’s an effective way to deploy capital in a manner that is safe, meaning that it’s relatively easy to understand the collateral that supports the loan and the revenue that comes off collateral in the form of rental.”

SPONSORED CONTENT

Business Cares: April 2024

In Colorado, 1 in 3 women, 1 in 3 men and 1 in 2 transgender individuals will experience an attempted or completed sexual assault in their lifetime. During April, we recognize Sexual Assault Awareness Month with the hopes of increasing conversations about this very important issue.

Now, institutions are hitting regulatory restrictions. As this cycle comes to fruition, Gorr said, banks are changing focus to a different type of lending strategy — commercial industrial lending, leasing efforts, owner-occupied real estate, working capital lines of credit, equipment loans or inventory loans — building on the growth that has been achieved so far.

“Basically, those loans that assist with the cash conversion cycle,” Gorr said.

On the other hand, Gorr notes that a local institution has a history of community knowledge and may be more comfortable with a larger transaction than say a national firm that does not understand the local market.

“We’re willing to invest more in our community,” he said. “But, we’re constrained because we’re not as big. We can’t have as significant of an impact because of our capital position.”

Gorr said capital is still readily available, though. There are a number of resources to be tapped.

“Boulder is a very desirable place to be and live,” he said. “We’re going to have to house the incoming residents.”

Commercial real estate activity is strongly correlated with local economy, said Gerard Nalezny, chairman and CEO of Verus Bank of Commerce in Fort Collins. Versus believes that commercial real estate is a sound thing to lend into.

“We continue to be aggressive in looking to expand our portfolio,” Nalezny said. “My suspicion is that we’re not alone. It’s a good market here.”

When there’s talk about people backing out of commercial real estate, it’s usually the large institutional players who follow whims more — they tend to get in and out of the market, Nalezny explained.

“For us, we’re pretty tied to Northern Colorado,” he said. “We lend when times are good, and we lend when times are bad. We had the highest growth rate during the recession. We’re always looking to grow.”

Community banks are closer to the ground, Nalezny noted. There are unique opportunities to be found in both the up and the down market.

“We live in a really cool place, and people will want to continue to be here, to move here, do business here, retire here,” he said. “I know that’s simplistic, but it’s a good market.”

Michael Cantwell, executive vice president at CBRE Group Inc., considers industry shifts to be business as usual.

“Banks all have the same level of regulations,” Cantwell said. “I don’t think it has negatively impacted lending by the local banks. It’s probably the size of the loans, meaning they aren’t lending as much money. In the past, maybe they loaned 80 percent of a project’s cost; today, maybe only 60.”

The commercial real estate industry is very cyclical, Cantwell said. When things are good, developers get enthusiastic, eventually there is overbuild, then a down cycle. Some borrowers have problems.

“It isn’t so much that we’re in a bubble. That suggests we artificially blew it up like in 2008 with the housing market. Commercial real estate is responding to real population growth, real job growth and a real demand for more space,” Cantwell said. “I wouldn’t consider it a bubble. It’s the natural cycle of doing business.”

If the banks are scaling back on lending, that means the developer needs to have more equity.

“There’s nothing wrong with more equity,” he said. “It’s safer for everyone.”

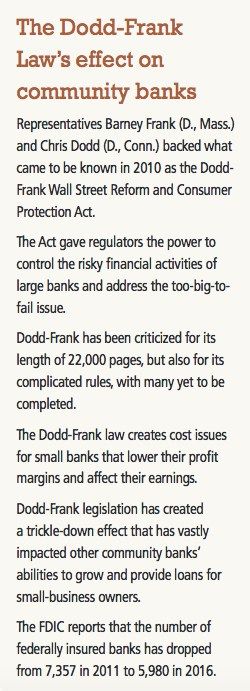

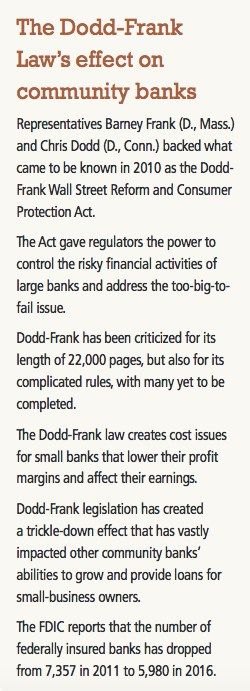

Banks right now are under pressure from their regulators to cut back on their exposure to commercial real estate. Cantwell explained that because Dodd-Frank considers that to be riskier than a fully leased development, they are requiring banks to reserve a lot more money against those loans — in case of loss. It discourages banks from making those kinds of loans.

The Dodd-Frank Wall Street Reform and Consumer Protection Act is a comprehensive piece of financial regulation born out of the Great Recession of 2008, designed to ensure that a financial crisis like that won’t happen again.

“When money is sitting in a bank reserve, it’s just idle money there,” Cantwell said. “You can’t make any money on it.”

Basel III, an international regulatory framework for banks, is also setting standards so banks worldwide have similar reserve requirements and consistent standards of lending.

“It’s subtle, but the banks are putting a lot of pressure to avoid HVCRE exposures,” Cantwell said.

The HVCRE regulation within the Basel III capital requirements mandates that, in order to be exempt from an HVCRE designation, borrowers who originate commercial acquisition, development and construction loans must meet a 15 percent equity requirement, and the leverage on such loans cannot exceed 80 percent of the estimated completed value of the project. If these conditions are not met, the loans will be subject to a 150 percent risk weight requirement — an increase from the previous 100 percent requirement.

“Think about a graduated risk profile,” he said. “Construction loans have the highest degree of risk, and then as you come down to commercial real estate that’s fully leased, that’s probably the least risky. Loans on property where all the leases expire next year, that probably falls somewhere in the middle.”

First Western Trust’s Gorr also believes in the power of the cycle.

“If you have an expansive portfolio of commercial or residential investment in this state,” Gorr said, “you can really impact your bottom line by taking it from the low borrowing cost, ride the wave of increasing rents, watch rates go up incrementally, then refinance your debt portfolio half a percent to one percent. That’s a significant benefit to your bottom line.”

In a White House meeting with members of the Independent Community Bankers of America, May 1, President Donald Trump said he is working to “roll back burdensome regulations” such as those created by the Dodd-Frank financial regulatory law and assured small bankers Monday that he’s committed to cutting red tape imposed on them.

Vice President Mike Pence added, “Dodd-Frank’s days are numbered.”

Despite reports of shrinking commercial real estate lending opportunities, the industry in Northern Colorado is robust, according to bankers in the region.

Matt Gorr, chairman of First Western Trust in Boulder, said the economy is seeing a number of financial institutions in the commercial real estate marketplace nearing capital restriction levels, which then is going to diminish the opportunity to fund loans as readily as they have been funded since the Great Recession.

“Financial institutions specific to our market in Boulder and Boulder County have been able to…

THIS ARTICLE IS FOR SUBSCRIBERS ONLY

Continue reading for less than $3 per week!

Get a month of award-winning local business news, trends and insights

Access award-winning content today!